When I talk to customers about their credit score, I begin by explaining how a credit score is calculated. With that background, they can determine if a new loan or signing up for a new credit card will improve their credit score or make it worse.

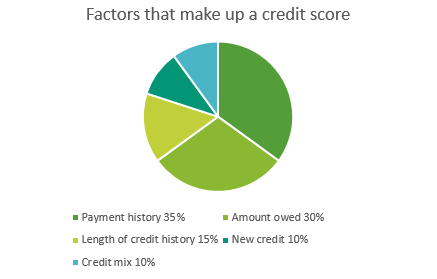

Credit scoring services like Experian and FICO use these factors when coming up with individual scores:

The Good Side of New Credit

Note that “new credit” is only rated at 10% of the total score. But a credit score is as unique as each of us, so when this 10% is weighted against other factors, it could have a significant effect – either to the positive or negative – on a score.

A new line of credit can help mix up the type of credit accounts someone has, favorably increasing the "credit mix" factor of a credit score. It shows lenders how people can manage different kinds of credit, which can lower their risk of lending money.

When opening a new credit card account, this could, initially, lower a score. But if the card isn’t used, this can, over time, increase a credit score because while the credit is available, it’s NOT being used. This can be an indication of good financial management that’s figured into the overall score.

Opening new credit also can help poor scores improve. Pay bills on time, and the score will increase over time.

The Bad Side of New Credit

When applying for new credit card or loan, the issuing company will take a look at a credit report by running an “inquiry” with one of the credit agencies. This single inquiry could lower your score by a few points.

A new line of credit will come into play when the credit agency scores the length of a credit history. This part of the score is made up of the "oldest" credit account and the average of all other accounts. Opening new credit lowers the average age of the total accounts. This, in effect, lowers the length of credit history and, as a result, a credit score.

If the new credit line isn’t used, then it can have a positive effect on a score. But most people apply for credit with the plan to use it. So once the credit is used, the “amount owed” component of a credit score could take a hit. The amount is the ratio of credit balances to credit limits. Usually, the less credit is used, the higher a credit score. But when the credit’s used, the closer someone gets to their credit limit. This often results in a lower credit score.

Home Buying: An Especially Bad Time to Open a New Line of Credit

Your credit score plays a huge role in your ability to get a mortgage loan and what the interest rate will be for that loan. The better your score, the better rate the bank can offer knowing there’s less risk of you not being able to pay back that loan.

INB requests a credit score from the credit agency when customers ask for a pre-qualification letter for a home loan. This triggers what is known as a “soft” credit inquiry. We aren’t pulling the full report, and the credit score isn’t affected. When the customer is ready to buy, we run a “hard” inquiry.

If someone applies for other credit between the soft and hard inquiry, the credit score could change. The change could be significant enough to affect loan qualification. That’s why I always tell my clients not to apply for any new credit while they’re home shopping. We don’t want any changes between pre-qualification and the time to buy.

If you need help understanding your credit score, don’t hesitate reaching out to me.