Your annual Escrow Analysis Statement provides details about your escrow account and changes to your monthly escrow payment. You will receive this statement annually on the anniversary date of your mortgage loan. Please review this statement carefully. If you find discrepancies or have any questions, please contact the INB Loan Servicing team at 217-747-8633.

Important reminders on Why Escrow-related Bills Can Change Over Time

If you have a fixed rate mortgage loan, the principal and interest portion of your monthly payment will not change. Payment changes are driven by changes in the escrow portion of your payment.

- Monthly payments will increase even if you pay the entire escrow shortage. Even if you pay the full escrow shortage resulting from last year’s escrow payments, an increase in your projected insurance premiums and/or real estate tax bill will mean an increased payment in upcoming months.

- Real estate taxes can increase based on property reassessments, a change in local tax rates, special assessments, etc. Contact your local tax office for questions regarding your real estate taxes.

- Homeowner insurance premiums can change due to changes in coverage, property values, rates, etc. Please contact your insurance agent with questions about your premiums.

How to read your statement

How to read your statement

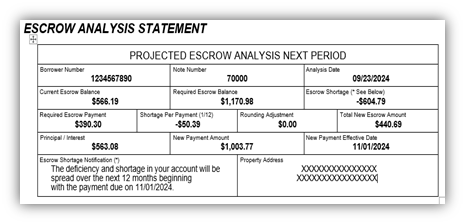

The “Projected Escrow Analysis Next Period” section gives you a summary of the key escrow information and changes:

- Date of the escrow analysis

- Escrow shortage/deficiency or overage amount

- Total new escrow payment amount

- Total new mortgage payment amount

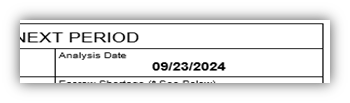

Analysis Date

The analysis date indicates when your escrow account was analyzed. This will be done every year on the anniversary month of your mortgage loan. If, during the course of the year, you change insurance companies or have your policy re-written, you may contact us to discuss running a new analysis based on the new insurance premium information.

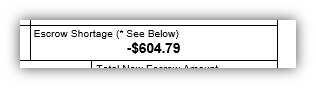

Escrow Shortage, Overage, or Deficiency Amount

An escrow shortage is the amount by which the escrow balance falls short of the required cushion amount, while an escrow overage is the amount by which the balance exceeds the cushion amount. An escrow deficiency is the amount by which the account has fallen below 0.

- Overages of $50 or less are used to reduce the monthly amount of escrow funds due, while overages greater than $50 are refunded to you.

- Shortages and deficiencies can be paid in one lump sum or spread over the next 12 monthly payments. If you do nothing, the shortage will be spread over the next 12 months beginning with the next monthly payment due.

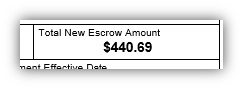

Total New Escrow Amount

The Total New Escrow Amount represents the new required amount for the escrow portion of your monthly payment. This is calculated by spreading the shortage over 12 months and adding that to your existing escrow payment.

New Payment Amount & New Payment Effective Date

The New Payment Amount represents your new monthly required mortgage payment: principal, interest, and the new escrow portion. The New Payment Effective Date indicates when the new mortgage payment amount begins.

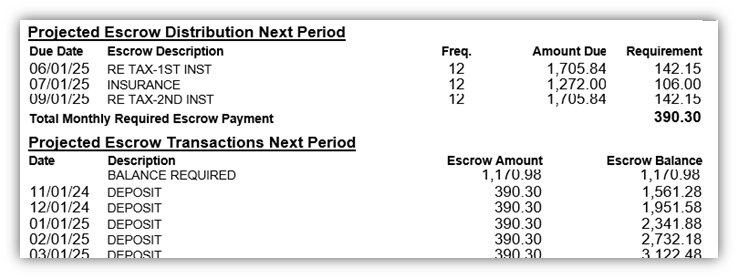

Projected Escrow Distribution & Transactions Next Period

We are required by federal law to analyze your account each year to determine whether the current balance and the amount of money we collect each month is appropriate based on the bills we expect to pay over the next 12 months.

This section contains projections of escrow activity for the coming year, inclusive of monthly payments into the escrow account and escrow disbursements out of the account based on last year’s activity. Please note: Any increase in property taxes or insurance premiums during the year could result in an escrow shortage or deficiency the following year.

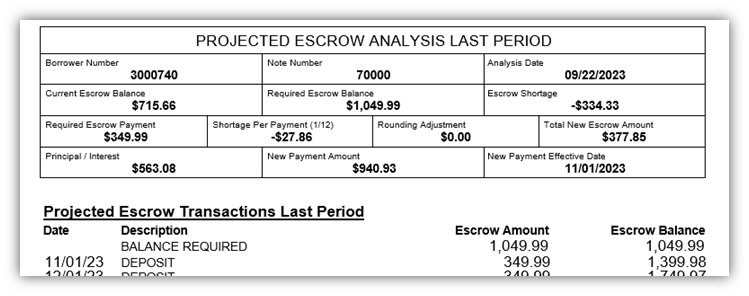

Projected Escrow Analysis & Transactions LAST Period

This section shows monthly transaction details of payments to and disbursements from your escrow account since the last escrow analysis date.